Car Insurance in Australia: Everything You Need to Know to Protect Your Ride and Save Money

What Is Car Insurance?

Car insurance is a legally required service in Australia that provides financial protection against damages or injuries caused in a car accident. Whether you’re a new driver or a seasoned one, it’s crucial to understand that this isn’t just about protecting your vehicle.

This type of insurance helps cover the costs related to property damage, medical bills, and even legal fees in some cases.

In Australia, car insurance operates under different levels, with various options depending on your needs. It’s important to know the basics, especially since not having proper coverage can lead to significant out-of-pocket expenses.

Who Needs Car Insurance?

In Australia, anyone who owns or drives a vehicle is legally required to have at least Compulsory Third Party (CTP) insurance. This covers injuries to other people in the event of an accident.

Even if you don’t drive often, or you think your car is not valuable, having insurance is a mandatory requirement and offers you peace of mind.

CTP might cover basic needs, but depending on how often you drive, where you park, and your overall financial situation, you might need more comprehensive coverage. From people who commute daily to those who only use their vehicle occasionally, car insurance is essential for all car owners.

Types of Car Insurance: Which One Is the Best for You?

There are several types of car insurance in Australia. Choosing the right one depends on your specific circumstances, such as the value of your car, your driving habits, and your budget.

- Compulsory Third Party (CTP) Insurance: This is mandatory in Australia and only covers personal injuries caused to others in an accident. It doesn’t cover damage to other vehicles or property.

- Third Party Property Insurance: This option covers damage to someone else’s property, such as their car or fence, but not your own vehicle.

- Third Party, Fire and Theft: Provides the same coverage as Third Party Property Insurance, but also includes protection if your car is stolen or damaged by fire.

- Comprehensive Car Insurance: The highest level of coverage, this policy covers damages to both your vehicle and other people’s property. It also covers incidents like theft, fire, and natural disasters. Although it’s the most expensive option, it offers the most extensive protection.

Choosing the best insurance depends on several factors, including your budget, the value of your car, and how frequently you drive. For newer cars, comprehensive insurance is often recommended, while older, less valuable vehicles might be better suited to Third Party Property coverage.

How to Lower Your Car Insurance Premiums

Lowering your car insurance premiums may seem challenging, but there are several straightforward strategies you can use to save money. The first tip is to always compare quotes from different insurers.

Prices can vary significantly, and doing some research can lead to substantial savings. Additionally, increasing your excess (the amount you pay upfront if you make a claim) can lower your monthly premium, though you need to be prepared to cover the excess in case of an incident.

Another way to reduce your premium is by securing your vehicle. Cars equipped with alarms, immobilisers, or parked in secure locations tend to have lower premiums, as they are considered less risky in terms of theft or damage.

It’s also important to review your coverage regularly to ensure you’re not paying for protection you don’t need. For instance, if you have an older vehicle, third-party insurance may be more appropriate than comprehensive coverage.

Insurers also often offer a no-claims bonus to drivers with a clean driving history, which can lead to lower premiums over time. Finally, paying your premium annually instead of monthly can help you avoid extra fees, saving you money in the long run.

What Does Car Insurance Cover (and What It Doesn’t)?

Understanding what your car insurance covers can help you avoid unpleasant surprises. Car insurance typically covers damage to your vehicle in the event of an accident, as well as damage caused to other people’s property, depending on the policy you’ve chosen.

If you have comprehensive coverage, your policy will also cover incidents like theft, fire, and natural disasters. Additionally, Compulsory Third Party (CTP) insurance in Australia covers legal liability for injuries caused to others in a road accident.

However, there are several things car insurance doesn’t cover, depending on your policy. If you only have third-party insurance, your policy won’t cover damage to your own vehicle. Similarly, mechanical breakdowns not caused by an accident are not covered.

Personal belongings left in the car, such as phones or laptops, usually aren’t covered unless you have an add-on policy that includes such items. Importantly, if you’re found driving under the influence of alcohol or drugs, your insurer is unlikely to pay for any damages or claims.

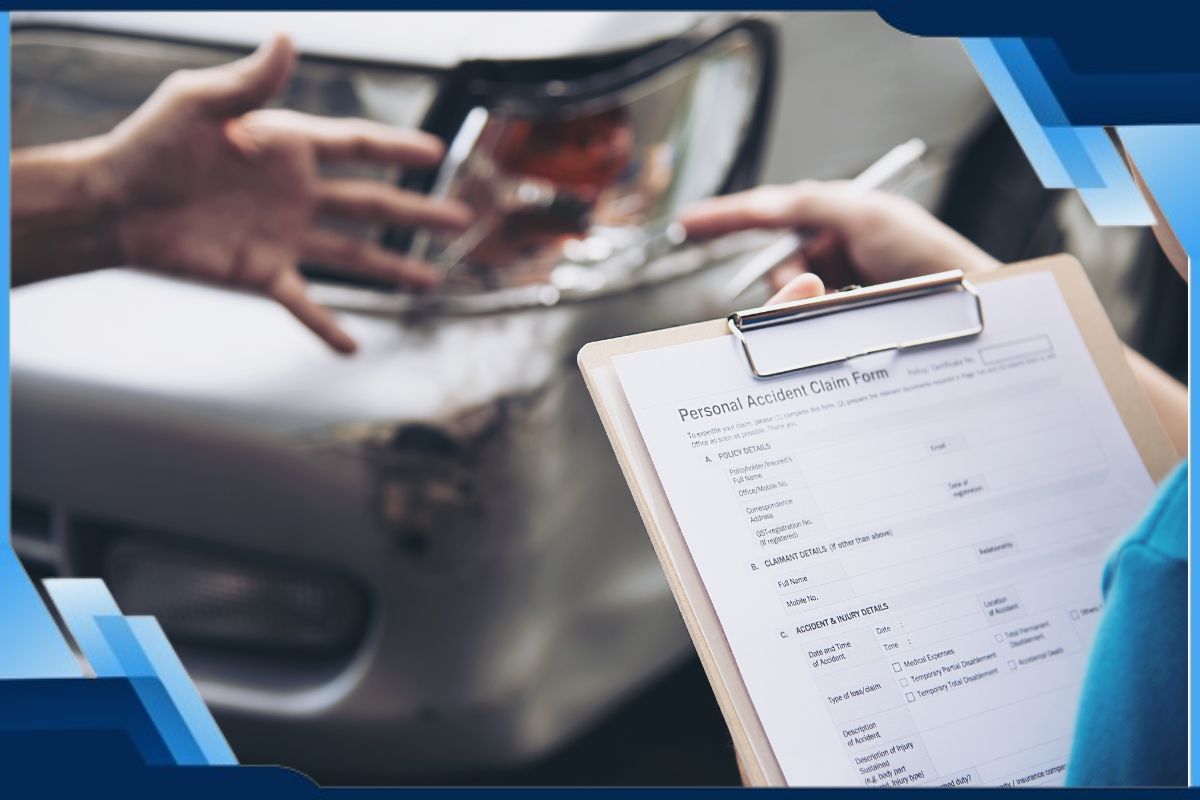

What to Do After a Car Accident: Step-by-Step Guide

In the event of a car accident, it’s important to stay calm and follow a clear set of steps to ensure the safety of everyone involved and to streamline the insurance claims process. First, check for any injuries and call emergency services if necessary.

Ensuring the health and safety of everyone is the top priority. If the accident is minor and no one is seriously injured, move your vehicle to a safer spot to avoid causing further incidents.

Next, exchange information with the other driver. This should include names, contact details, insurance policy numbers, and vehicle registration numbers.

Be sure to document the accident scene by taking photos of the damage, the location, and any other relevant details that may be helpful during the claims process. Once you’ve gathered this information, contact your insurance company as soon as possible to report the accident and start the claim.

Common Car Insurance Myths: What You Should Know

There are many misconceptions about car insurance that can lead to confusion. One common myth is that older cars don’t need insurance.

While comprehensive coverage may not be necessary for older vehicles, it’s important to have at least third-party insurance to cover damage to other people’s property. Another myth is that the colour of your car can affect your insurance premium.

In reality, factors such as the make, model, and age of the vehicle play a much bigger role in determining your insurance costs than the colour of your car.

Some drivers also believe that their insurance policy covers everything, but it’s important to understand that all policies come with exclusions. For example, if you drive under the influence or if your car suffers mechanical issues that aren’t related to an accident, your insurance may not cover the resulting costs.

It’s essential to read and understand the terms of your policy to avoid these misconceptions.

How to Choose the Best Car Insurance for Your Needs and Budget

Choosing the right car insurance involves more than just looking at the price. Start by assessing your needs—how often do you drive, where do you park your car, and what’s the value of your vehicle?

These factors will help you determine the level of coverage that’s most appropriate for you. Next, set a budget for both your premium and excess, and try to find a balance between what you can afford monthly and how much you could pay in case of an accident.

It’s also wise to use comparison websites like Canstar and Compare the Market to get quotes from multiple providers. Customer reviews can also provide insight into how insurers handle claims and customer service, which is crucial in case you ever need to make a claim. Lastly, check for any available discounts. Many insurers offer multi-policy discounts if you bundle car insurance with other types of coverage, such as home or health insurance.

Examples of Companies Offering Car Insurance in Australia

When it comes to choosing a car insurance provider in Australia, there are several well-known companies and banks that offer a variety of coverage options tailored to different needs and budgets. Some of the popular providers include:

- NRMA Insurance: One of the most established insurance companies in Australia, NRMA offers a wide range of car insurance options, including comprehensive, third-party, and CTP coverage. They are known for their strong customer service and extensive network of service providers across the country.

- AAMI: AAMI is another major player in the Australian car insurance market, offering competitive rates and multiple types of coverage, including comprehensive, third-party, and fire and theft insurance. AAMI also offers multi-policy discounts and has a strong reputation for handling claims efficiently.

- RACV (Royal Automobile Club of Victoria): Operating primarily in Victoria, RACV provides a variety of car insurance options, along with roadside assistance services. They offer flexible coverage, which can be customised based on your needs.

- Allianz: Allianz is a global insurance provider that offers a broad range of car insurance products in Australia. They are known for their comprehensive policies and provide various options for both new and experienced drivers.

- Commonwealth Bank: One of the largest banks in Australia, Commonwealth Bank offers car insurance products in partnership with Hollard Insurance. Their policies include features like new car replacement, personal effects cover, and discounts for bundling policies.

- ANZ: Another major bank, ANZ, provides car insurance through QBE Insurance. Their options include comprehensive and third-party property insurance, with the added convenience of managing policies alongside your banking needs.

Car insurance is an essential part of owning a vehicle in Australia, offering peace of mind and financial protection. By understanding the different types of insurance, comparing providers, and making informed choices, you can find the best coverage for your needs and budget.

Make sure to regularly review your policy and keep your coverage updated as your circumstances change.

About the author

As a journalist passionate about digital content, I create strategic texts for various niches. I believe in the power of clear and accessible information, and my goal is to simplify complex topics while promoting free access to knowledge that can improve people’s everyday lives.